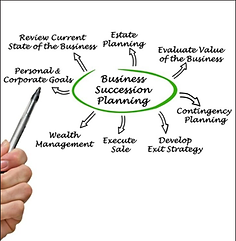

When do you need a business succession plan?

The overriding answer is, in almost every conceivable case, always. Protecting your business and operations, and safeguarding future owners and heirs, should be a top priority when determining how your business will operate and under whose leadership when you are no longer the owner. You should review your business succession plan at least annually and when changes in tax laws, valuation, industry developments, or family dynamics have occurred. A business succession plan allows a business owner to hand over their business in the event of the owner’s exit due to any number of reasons including retirement, disability, or death and allows the business owner or owners to control what happens to the business. A properly developed plan for any type of business should have at a minimum a well drafted agreement including provisions regarding an owner’s exit and how it will be managed. If an operating agreement already exists without these provisions, it is possible to execute a buy/sell agreement to indicate the wishes of the owners/members/shareholders. One common misconception of business owners is that a business entity is separate from their personal estate. However, this isn’t the case, and you can’t ignore the impact that a business may have on your heirs upon your death. Even if a business is not being left to surviving heirs, it’s imperative that this is outlined clearly in your final plans. In the state of Texas, failure to plan properly will result in your last will and testament determining the disposition of your business interests. If you die without a will and no business succession plan, then your business interests will pass per Texas statute, and this may be far from what you envisioned for your life’s work. Regardless of who you wish to take the reins of your business upon your departure, there are several key things to determine at the onset of the planning process: Determine a timeline for when the succession should take place, either on a predetermined date or in the event of death or disability Select a successor: If no specific party has been identified consider family members or other potential candidates Document your standard operating procedures, including an organizational chart, employee handbook, operations manual, and any other recurring meetings or processes to help you determine qualified candidates Value your business, optimally engaging the assistance of a professional to establish your company’s worth Define a specific path outlining how a successor may purchase the business, including options such as life insurance, loan, or seller financing Once you determine who will be taking over your business and how that transfer will occur, it’s time to engage the expertise of a professional who can execute the proper paperwork to make sure that the business will seamlessly transfer to the intended new owner(s). To help you review or create a succession plan for your business, contact Angela Odensky at The Law Office of Angela Odensky at info@odenskylaw.com.

What is a business succession plan? – Law Office of Angela Odensky

In the simplest terms, a business succession plan allows a business owner to pass on leadership roles or to hand over their business in the event of an owner’s exit due to a variety of reasons including retirement, disability, or death — allowing the business owner(s) to control what happens to the business. Whether an owner chooses to leave his business to his family, key employees, or seek an outside third party to purchase, a clear-cut plan outlines the owner’s intentions and follows set wishes. A business succession plan for any type of business should have, at a minimum, a well drafted agreement including provisions regarding an owner’s exit and how it will be managed. If an operating agreement already exists without these provisions, it’s possible to execute a buy/sell agreement to indicate the wishes of the owners/members/shareholders. Ideally, the planning process should initiate at least five years before a planned retirement. In the instance of a non-planned exit of an owner due to death or physical or mentally disability, a business succession plan guides logistical and financial decisions regarding leadership and operations going forward. Factors involving business succession planning and strategy that go beyond transferring ownership include evaluating day-to-day operations, review of facilities and/or locations, analyzing the potential impact of business interruption, and a plan to protect data and infrastructure. What Happens Without a Plan? In Texas, if you do not have an agreement that outlines your exit plans, then a last will and testament will control the disposition of your business interests. If you die without either a will or a business succession plan, then your business interests pass per Texas statute. This could leave the future of your business in jeopardy, and may cause ongoing issues with surviving business owners and heirs. Safeguarding Your Business Assets Transitioning your business should be handled by an experienced third party who understands the nuances of this often complicated process and who can efficiently incorporate your exit strategy so that your business continues as you intend. Planning properly avoids common and some not so common scenarios that can make business succession difficult and cause unnecessary and costly delays and complications down the road. Contact Angela Odensky at The Law Office of Angela Odensky at info@odenskylaw.com to discuss your business succession strategy now.

Planning 101 – Law Office of Angela Odensky

Business succession planning can involve various legal vehicles and documents, as it is tailored to the type of business, ownership formation, existing succession documents, and the succession intent of current owners. There are multiple ways to plan for and legally guide your final succession plan to ensure that your wishes are observed. What documents do I need for business succession planning? Start with a well-drafted agreement that might include provisions regarding an owner’s exit and how it will be managed. This is true for any type of business entity. If an operating agreement already exists without these provisions, it’s possible to execute a buy/sell agreement to indicate the wishes of the owners/members/shareholders. What if I have an operating agreement in place, but it doesn’t address the exit of owner(s)? A well-drafted agreement for any type of business can include provisions regarding management of an owner’s exit. If an operating agreement already exists without these provisions, it’s possible to execute a buy/sell agreement to indicate the wishes of the owners/members/shareholders. How often should I review my business succession plan? You should review your business succession plan at least annually and certainly when changes in tax laws, valuation, industry developments, or family dynamics occur. What are some common ways to transfer ownership of a business? – Co-owner: Selling shares or ownership interests to an existing co-owner – Heir: Passing ownership interests to a family member – Key employee: Selling to a key employee – Outside party: Selling to an entrepreneur outside the organization – Company: For a business with multiple owners, ownership interests can be sold back to the company and distributed to remaining owners These are just some of the vehicles available to guide your succession strategy. An experienced and knowledgeable professional can help you explore options and make certain the proper paperwork governs your plans. Contact Angela Odensky at The Law Office of Angela Odensky at info@odenskylaw.com to ensure your business continues per your wishes.

All in the Family – Law Office of Angela Odensky

Only 30% of businesses get passed on to family upon the death of an owner — for many reasons including non-interest of family members, family members not skilled to run the business, or divergent opinions about how the business will be run and who will lead it. The most important consideration in any planning is the people involved and for small, family-owned businesses, it’s crucial to know whether the next generation is interested in carrying on the business. Establishing whether one or all children want to continue the business helps guide your plan and protect the interests of your heirs. With family businesses, a number of factors must be considered to protect the inherited asset. Planning helps to consider various scenarios such as whether one child wants to keep the business while others may desire a cash payout and what to do in the event that there isn’t money for a payout. A professional can help you address these issues as well as alert you to the benefits of sound succession planning including transferring a business to eager family members, with the following potential benefits: Minimizing tax costs Holding business assets in protected structures Continuing the cash flow to the business owner post succession Ensuring a successful transition of management to the family members With small businesses, planning early sets the stage for future succession and addresses possible pitfalls. For instance, consider a couple launching a brand-new business that they hope to pass on to their (currently) young children. Though their retirement may be many years in the future, the couple should plan now to protect their legacy. The following documents should be in place: An operating agreement Establish partners of the LLC Allowing for one child to assume business in the event that the other child(ren) no longer wish to be involved Obtain insurance policy on all owners Have buy-sell agreements Handing over the reins of a successful enterprise can be highly attractive for a business owner and the potential new owner, and choosing a family member(s) as your successor is a more viable option when children or other family members are already working within the organization. If you are considering succession for your business entity, timely planning with professional guidance can protect your business and its future. Contact Angela Odensky at The Law Office of Angela Odensky at info@odenskylaw.com.

Focus On: Business Succession Planning

Welcome to FOCUS ON, The Law Office of Angela Odensky’s newsletter designed to provide critical information you need to know in order to plan for your future – both for yourself and those you love most. We kick off this quarter with an edition exploring the many facets of business succession planning including retirement, ownership transition, assumption by heirs, or death/disability of key owner(s). WHAT IS A BUSINESS SUCCESSION PLAN? A business succession plan allows a business owner to pass on leadership roles or to hand over their business in the event of an owner’s exit due to a variety of reasons including retirement, disability, or death — allowing the business owner to control what happens to the business. For a business owner, a succession plan often goes hand-in-hand with comprehensive estate planning. Whether an owner chooses to leave his business to his family, key employees, or seeks an outside third party to purchase, a clear-cut, pre-transition plan outlines the owner’s intentions. If a business owner dies without proper planning and no directives in place, disposition of the business interests will be dictated by a last will and testament. If there is no will or a business succession plan in place, the business interests will pass per Texas statute, which may be in direct conflict with the business owner’s original intentions. WHY IS A BUSINESS SUCCESSION PLAN SO IMPORTANT? A strategic and successful business succession plan should cover both planned and unplanned occurrences. While you should seek a business succession plan at least five years prior to your planned business exit, a strategy to include death, disability, or incapacitation should also be in place for the unexpected. An attorney experienced in creating business succession planning to address multiple possible scenarios ensures your wishes are followed regarding the future of your business for any reason. Whether an owner is transitioning the business to family or employees or seeks to sell outright, timely planning allows for the optimum setup to protect assets. At the basis of a properly structured business succession plan are key documents that an experienced attorney can either create or amend including operating agreements that name partners of the LLC; outline ownership transition (especially critical for business entities with multiple and/or non-related owners); establish buy-out terms; set terms for one child to assume the business in the event that the other child(ren) no longer wish to be involved; create viable buy-sell agreements; protect owners by establishing insurance policy requirements for all owners/key employees; and set terms for withdrawal in the event of retirement, disability, or death. CASE STUDY: THE LACK OF A BUSINESS SUCCESSION PLAN POSES SIGNIFICANT ISSUES FOR A DECADES-OLD FIRM A recent matter handled by the firm involves three colleagues who shared a vision over three decades ago by starting their own thriving company. Over the years their friendship and working relationship remains strong, but their visions have diverged. One partner essentially retired five years ago while still pulling full distributions; one partner is ready to retire now and struggles with the next best steps to achieve this; and the final partner has no plans to retire for several more years and wants to keep the status quo. The common vision shared by the three colleagues did not include planning for its future. At no time in the decades together did they enter into an operating agreement that would outline exactly how the company would handle retirement of its primary members. Now, as they age, the only concern isn’t just how to retire, it’s what happens if one of them dies and what authority a spouse inheriting part of the business will have on the remaining original members. Though that can be answered by state law, all of these questions and concerns can instead be addressed by the business via a well-drafted operating agreement. And, while nothing brings more satisfaction and pride than building a successful business with people you admire and respect, protecting that business with a thorough plan that anticipates its success and lays the foundation to create a legacy should be a priority for all business ventures. Business succession and estate planning strategies can help guide you as you determine your individual business exit, initial public offering, acquisition, or succession planning. ALL IN THE FAMILY The most important consideration in any business planning is the people involved. For small, family-owned businesses, it’s crucial to know whether the next generation is interested in maintaining the business and in what capacity. Establishing whether one or all children want to continue the business helps guide your plan and protect the interests of all of your heirs. While only 30% of businesses pass down to the next generation, there are many benefits to an established business entity when ownership transfers within the family. Benefits of continued familial ownership include minimizing tax costs; holding business assets in protected structures; continuing business cash flow post-succession; and ensuring a successful transition to intended family members. In addition to the above benefits, maintaining ownership within a family strengthens and reinforces the foundational roots of a business and can keep the business thriving. Take for instance a scenario where not all children are necessarily interested in being a part of the family business, yet the family’s estate is wrapped up in the business. Business succession planning should be done in conjunction with traditional estate planning allowing that each family is different and the best way to determine the division of the estate/business will depend on the overall family dynamic. It’s crucial to understand that the children will not ‘just work it out amongst themselves.’ When it comes to the division of assets, it’s best to take the reins and set your children up for future success. Handing over the reins of a successful enterprise can be highly attractive for an owner and a potential new owner. Choosing a family member(s) as your successor is a more viable option when children or other family members are already working within the organization. Business succession